Annual

Report

2021

Report

2021

Findeks is a financial services platform launched by KKB in 2014 with the mission of allowing financial life in Turkey to better function. To that end, Findeks provides individuals and corporations alike with access to credibility indicators which the financial sector has used for many years, thus ensuring transparency bringing financial management and monitoring within the reach of everyone.

Findeks aims to help real sector companies get to know each other financially, improve their risk-taking and risk-management abilities, protect their capital and reputation and expand their sales and competitiveness. In light of the advantages provided by Findeks services, companies are able to significantly improve the quality of their assets and contribute to the financial environment and the financial industry in Turkey.

In addition to basic products such as the Findeks Credit Rating, the Findeks Risk Report, the Findeks Cheque Report and the Findeks QR Code Cheque Report, which cover all major financial indicators, KKB also filled important gaps with value-added products such as the “Findeks Rating Consultancy” which provides expert advice on how to improve credit scores, the “Findeks Tracer” which allows individuals to find out whether their financial and personal information has been made available online through fraudulent sites, the “Findeks Warning Service” which provides alerts on changes to credit card limits and debts with all banks, and the “Findeks Credit Rating” which provides notification of applications for credit which have been filed.

QR Code Cheque System introduced by Findeks became mandatory for all cheques by law on 1 January 2017. The QR Code Cheque System is intended to establish a more transparent and secure environment for trade, while increasing production, employment, prosperity and trade volume. A key tool for access to Findeks services, the Findeks Mobile application was renewed in 2019. The renewed Findeks Mobile provides a next-generation home page where users can easily monitor their credit ratings and credit products at all banks. Featuring a design that facilitates access to products and service offerings, the app also offers a superior customer experience for Findeks members.

Findeks, which offers a wide range of products to its users, reaches its customers through a number of different channels including the mobile application, internet branch, website, customer communications center, banks and strategic business partners. Work is underway to further develop these channels.

444 4 552

www.findeks.com

www.facebook.com/Findeks

www.twitter.com/Findeks

www.instagram.com/findeks

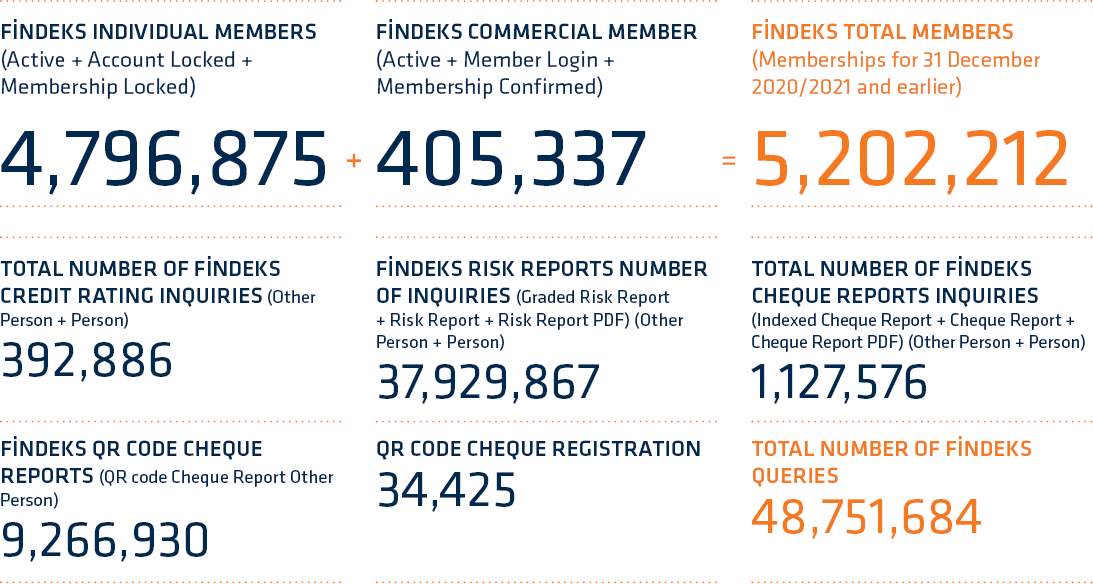

FİNDEKS CREDIT RATING

The Findeks Credit Rating has served as a reference for banks in their lending decisions for many years. This score is calculated based on the credit limit, risk and payment history related to personal loans which individual customers have obtained from banks and financial institutions, credit card and overdraft accounts, new credit openings and the frequency of credit usage.

The Findeks Credit Rating functions a summary of the Findeks Risk Report. Banks and other financial institutions take into consideration the credit rating and the payment history while assessing loan applications and managing their consumer loan portfolio. They can also predict future payment performance.

The Findeks Credit Rating is used by the real sector as a powerful supporting tool in decision making. With the Findeks Credit Rating, institutions improve their ability to offer customers the right product at the right price, boost automation in decision processes, reduce operational costs and increase customer satisfaction and profitability. Individuals, on the other hand, may use their Findeks Credit Rating as a strong reference to demonstrate their debt repayment performance to the individuals and institutions with which they will have a debt relationship.

FİNDEKS RISK REPORT

The Findeks Risk Report is a report in which credit, credit card and overdraft accounts in banks can be reviewed collectively, where total debt and limit information in banks can be accessed and payment habits tracked. The report covers housing loans, auto loans and consumer loans, credit cards, overdraft accounts and commercial loans. All information pertaining to these products is submitted to the TBB Risk Center by financial institutions on a regular basis, compiled by KKB and included in the Findeks Risk Report. As a result, individuals and the real sector are able to access information regarding the credit products of all banks in a single report. The Findeks Risk Report allows users to view their own financial information in detail. They may also view the financial performance of other persons or enterprises where they have their approval to do so.

Risk Reports ensure a safe environment for trade, enabling viewing of the repayment history in trade relations and thus the payment habits of the other party, allowing precautionary measures to be taken against accounts receivable risk.

FİNDEKS CHEQUE REPORT

The Findeks Cheque Report provides a summary of the payment habits of an individual or institution. If a cheque bearer obtains approval from the drawer, then may track the cheque payment history of that drawer. The Findeks Cheque Report also contains information regarding all banks which offer cheques in Turkey. The data contained in these reports relate to the period after 2009 for bounced cheques and after 2007 for paid cheques. Data is updated daily.

FİNDEKS CHEQUE INDEX

The Findeks Cheque Index is calculated based on the past cheque payment behavior of legal entities and natural persons. The main factors affecting this index include the frequency of cheques drawn over the last 36 months, their date proximity, amounts, and number. The Findeks Cheque Index ranges from 0 to 1,000 points. In the Findeks Cheque Index, where an issuer fails to pay any of the cheques, they will receive a score of 0; where they pay all of the cheques when due, then they receive a score of 1,000 points. However, if even one cheque has bounced and remains unpaid, the Findeks Cheque Index will be between 1 and 500 points. Where there have been bounced cheques but any outstanding balance has been paid later, the Findeks Cheque Index will be between 501 and 999 points. The Findeks Cheque Index provides an idea regarding the cheque payment habits of an individual or an enterprise.

FİNDEKS QR CODE CHEQUE SYSTEM

This system allows an issuer’s past cheque payment status to be viewed, without an approval process or checking for potential forgery of the cheque, by scanning the QR Code on the Findeks Mobile Application. The QR code is then produced upon the request of the customers from the bank, along with legal enforcement functionality, and without the need for consent.

As required by law, all cheques have been required to have QR codes and be registered in the Findeks QR Code Cheque System with effect from 1 January 2017.

The Findeks QR Code Cheque System, which is the first and only one of its kind in the world, allows careful checks of the risks of receivables arising from payments made by cheque, along with information regarding the validity and authenticity of cheque within seconds.

FİNDEKS QR CODE CHEQUE REPORTS

The Findeks QR Code Cheque Report is a report where the details the cheque payment history of the issuer can be viewed through a QR code, which became mandatory with effect from 1 January 2017. This report also allows the information on the cheque leaves to be compared with the information in the system. Thanks to the Findeks QR Code Cheque Report, which can be obtained from the Findeks Mobile application, issuer information such as cheque payment performance, forward-term cheques and the number of open cheques can be accessed easily before the acceptance of cheques.

FİNDEKS QR CODE CHEQUE REGISTRATION SYSTEM

The Findeks QR Code Cheque Registration System aims to create a record based on the issuance date as soon as the bearer or endorser accepts the cheque. The Findeks QR Code Cheque Registration System is legally supported, and its use has been promoted since 1 January 2018.

Under the system, fraudulent cheque issuers are unable to lodge objections alleging that the signatory was not an authorized person of the institution on the date of collection for a cheque that is registered in the Findeks QR Code Cheque Registration system. Therefore, cheques registered in the cheque registration system may leave traces in the system on the date of registration.

FİNDEKS MONITORING SERVICE

The Findeks Mobile application, which was renewed in 2019, allows users to monitor the limit and debt status of their loans, credit cards and overdraft accounts as well as their payment performance and any changes in their credit rating at all banks on a daily basis. With the aim of reaching a wider audience through Findeks Mobile, this feature, which allows users to easily monitor their information, is offered to users free of charge for the first three days.

FİNDEKS WARNING SERVICE

Another feature which sets Findeks apart is the Findeks Warning Service, which provides instant notifications on any changes to the Findeks Credit Rating, credit card limit and debt status, or credit applications made. With this service, customers may keep their current finances under control and take action when necessary.

The Findeks Warning Service tracks these changes in accordance with the criteria set by customers and notifies them via SMS or email.

With Findeks Warning Service, alerts can be defined to the system, for example in the scope of the following cases, and a warning message is sent to the user:

FİNDEKS TRACER

The Findeks Tracer is another exclusive benefit provided to Findeks customers. The Tracer protects personal and sensitive data, including ID, contact, credit card information transmitted by the user by running extensive scans online, including the “dark web.” The user is promptly notified if such information is found on unreliable websites. The Findeks Tracer fills an important need in today’s world where sharing of personal and financial information is continuously increasing with the effect of digitalization, helping to meet a wide range of needs from business, shopping and education to socializing on the internet.

MY FİNDEKS RATING CONSULTANT

The Findeks Credit Rating Consultant system, which aims to create the necessary foresight for users to manage their own financial life and to establish commercial relations on solid foundations, brought with it the need for objective information on how to increase and maintain a credit rating.

The My Findeks Rating Consultant product offers personalized advice on how to increase the Findeks Credit Rating or how to maintain a high level rating.

LETTER OF GUARANTEE STATUS INQUIRY

The Letter of Guarantee Status Inquiry (LGSI) service allows customers to check the validity of a letter of guarantee without contacting the issuing bank. Using parameters such as “Bank Name,” “Branch Name,” “Letter of Guarantee Number,” “Amount,” “Currency Code” and “Expiry Date,” customers may perform an online check to find out whether a letter of guarantee has been issued and whether an active risk record exists for that letter of guarantee.